Interest Rate Uncertainty: Strategies & Direction

Canada Faces Economic Uncertainty as U.S. Trade Tensions Rise

As 2025 begins, anxiety looms over Canada’s economy following Donald Trump’s return to office. His proposed tariffs—potentially reaching 25% on Canadian and Mexican exports—threaten to disrupt key industries, weaken the Canadian dollar, and stifle economic growth.

Bank of Canada Governor Tiff Macklem has warned of severe consequences if trade tensions escalate, emphasizing that this isn’t a temporary shock but a fundamental shift in Canada’s economic trajectory. "Increased trade friction with the United States is a new reality," he stated. A prolonged trade conflict could significantly lower Canada’s long-term economic output, with no immediate rebound in sight.

According to Bank of Canada projections, exports could fall by 8.5% within a year, while business investment may shrink by nearly 12% due to rising costs and declining confidence. Job losses and inflationary pressures are expected, as 13% of Canada’s consumer price index is tied to U.S. imports. The weakened loonie would further drive up costs for Canadian consumers.

Although the Bank of Canada has been cutting interest rates, Macklem cautioned that monetary policy alone cannot offset the economic damage. While lower rates may help domestic demand, they won’t restore lost trade or prevent inflation.

Key sectors like oil, automotive, forestry, agriculture, aerospace, steel, and retail face severe disruptions. Alberta’s oil industry relies on U.S. refineries, and Ontario’s auto sector depends on cross-border supply chains, making tariffs especially damaging.

To mitigate long-term risks, Macklem stresses the need for structural reforms, such as reducing interprovincial trade barriers and expanding global market access. However, with uncertainty already deterring investment, Canada faces a difficult economic road ahead.

How the Overnight Rate Affects the Prime Rate?

The prime rate is typically 2.2% higher than the overnight rate. If the overnight rate is 3%, the prime rate would be 5.2%. Some banks predict the overnight rate could drop to 2% by year-end, bringing the prime rate down to 4.2%.

All variable-rate mortgages are tied to the prime rate, with or without a discount. Some adjust with rate changes, while others remain fixed. However, the lowest rate isn’t always the lowest cost—portability matters. Some lenders also charge three months’ interest based on the prime rate, not the discounted rate.

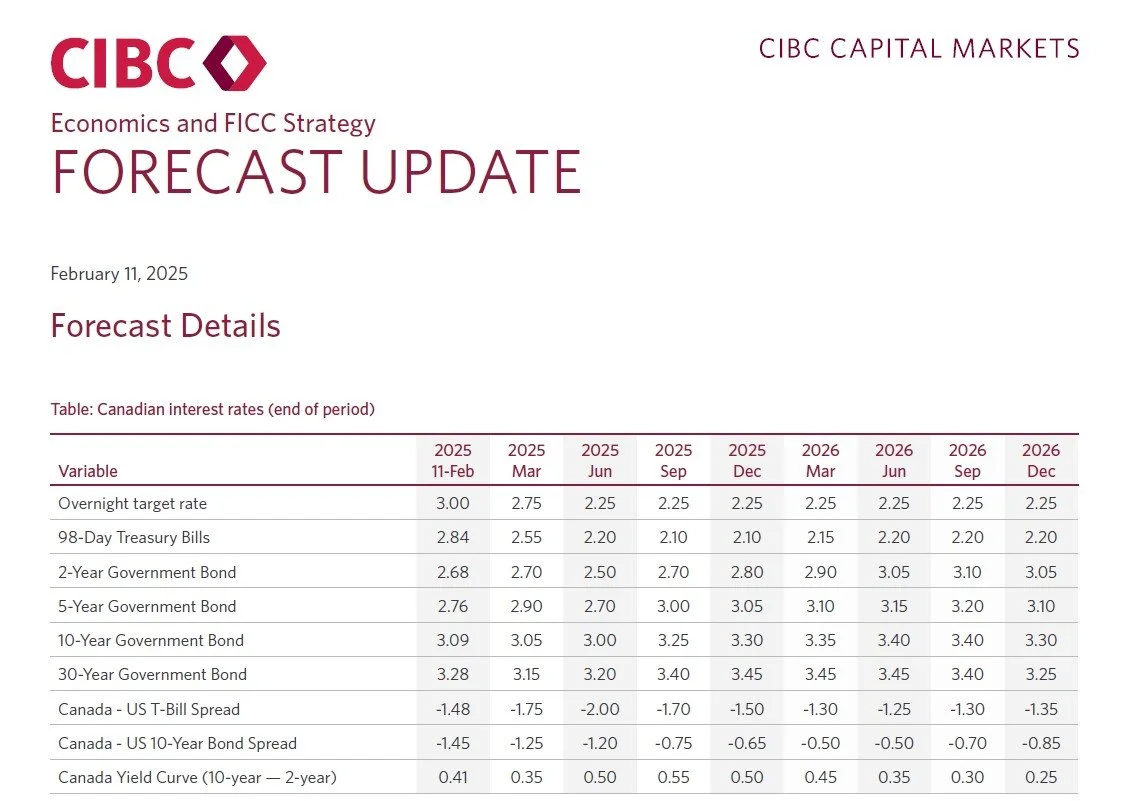

In its latest forecast, National Bank of Canada (NBC) predicts the BoC will cut its policy rate by 100 basis points (one percentage point) to 2.25% this year, before then hiking rates by 50 bps in 2026.

National Bank economist Tyler Schleich told Canadian Mortgage Trends that the anticipated hikes would follow a period where the BoC lowers its policy rate slightly below neutral to stimulate the economy.

“While not in recession, Canada’s GDP growth has been below potential for some time and thus we’ll need a period of GDP growth to run above potential to return the economy to its equilibrium,” Schleich explained.

“That’s why our forecast involves a year of the policy rate at 2.25%,” he added. “Once the economy picks back up and slack is absorbed, the BoC will be able to return the policy rate to neutral, which we view as 2.75%.” Link to the article

The Bank of Canada is analyzing multiple scenarios to determine appropriate monetary policy responses once tariff details emerge. Current analysis suggests the tariffs would likely have a net disinflationary effect, potentially leading to lower policy rates than otherwise planned. However, if the government chooses to support affected workers and industries through increased borrowing and spending, the overall effect could become inflationary.

Choosing Between Fixed and Variable Rates

When it comes to selecting a mortgage term, the choice between a variable or fixed rate ultimately depends on your risk tolerance and comfort level. Many clients are currently opting for variable-rate mortgages with a discount, allowing the flexibility to lock in a fixed rate later without any penalties. Others prefer the stability of a shorter fixed term, typically 3 years or less, for added peace of mind. Great article: Fixed vs. Variable Mortgages in a Shifting Rate Environment

Strategies to Minimize Mortgage Interest Costs:

1. Choose a Variable Rate with Flexibility

Select a variable rate with a discount and the option to switch to a fixed rate. Interest rates may rise temporarily but are expected to decline between Q3 2025 and Q2 2026. You can lock into a fixed rate later or continue with the variable rate.

2. Choose a Short Fixed Term (2–3 Years)

Lock into a short-term fixed rate with the expectation of securing a lower rate when renewing. This strategy works if rates drop as projected.

3. Lock into a Longer Term with Flexibility

Choose a long-term fixed rate and explore options like blend-and-extend with certain lenders to lower your rate over time. Alternatively, work with lenders that offer reasonable penalties for breaking your mortgage if lower rates become available.

If you have any questions or would like to explore your mortgage options further, please feel free to reach out. We’re here to help you navigate the mortgage landscape!